How do the estate, gift, and generation-skipping transfer taxes work?

The federal estate tax applies to the transfer of property at death. The gift tax applies to transfers made while a person is living. The generation-skipping transfer tax is an additional tax on a transfer of property that skips a generation.

The United States has taxed the estates of decedents since the creation of the modern personal income tax in 1916. Gifts have been taxed since 1924. In 1976, Congress enacted the generation-skipping transfer (GST) tax and linked all three taxes into a unified estate and gift tax.

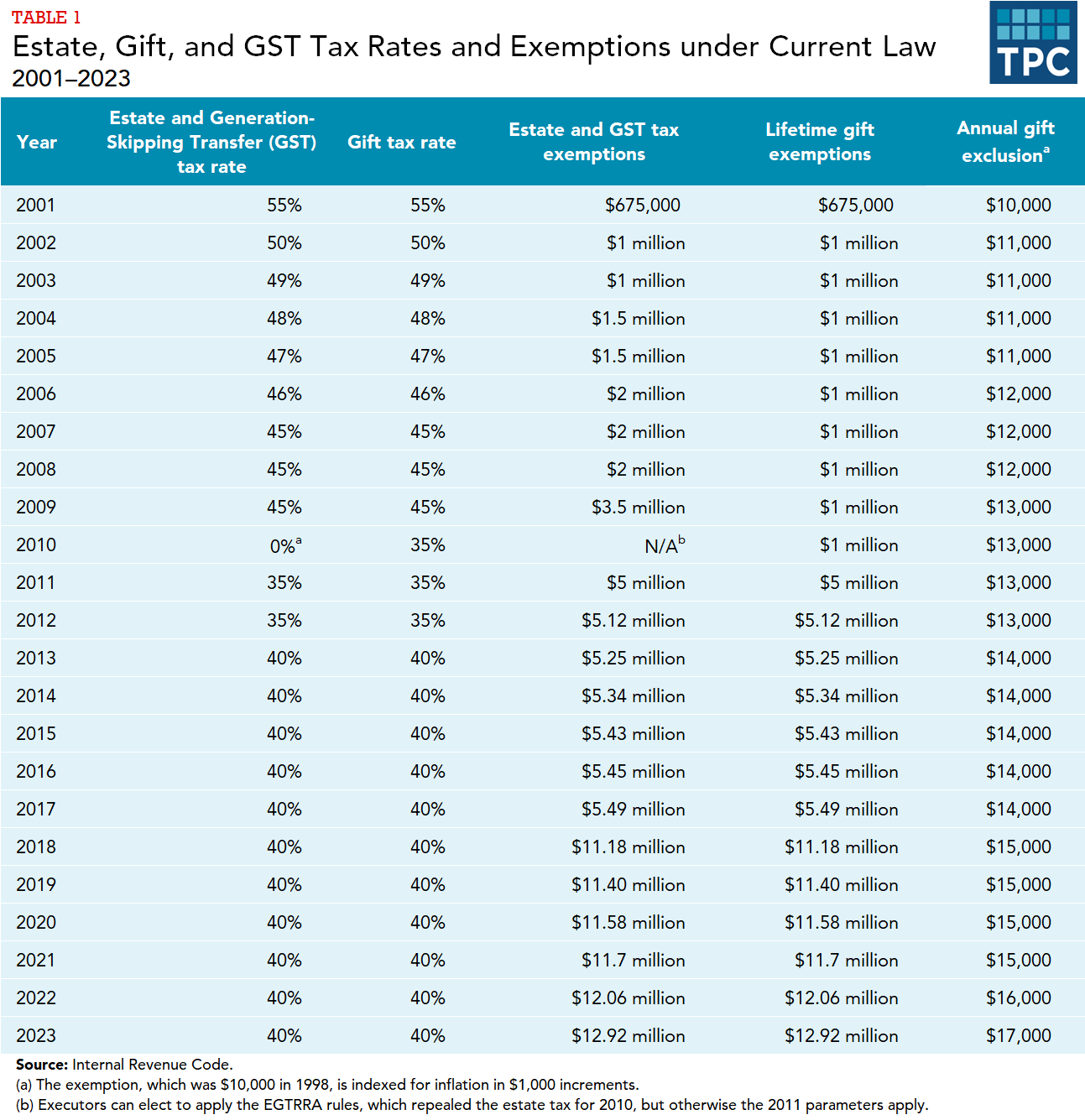

The tax applies to the portion of the estate’s value that exceeds an exemption level. The Tax Cuts and Jobs Act (TCJA) doubled the estate tax exemption to $11.18 million for singles and $22.36 million for married couples, but only for 2018 through 2025. The exemption level is indexed for inflation reaching $12.92 million in 2023 ($25.84 million for married couples). The taxable portion of an estate is subject to a flat 40-percent tax rate.

Tax rates and exemption levels have varied substantially over the past 25 years. Before the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA), the estate tax exemption was set at $675,000 and scheduled to gradually increase to $1 million. Estate tax rates ranged up to 55 percent, with an effective top rate of 60 percent. EGTRRA cut all three taxes sharply, but only through 2010. The act gradually phased out the estate and GST taxes and repealed both entirely for 2010, leaving only the gift tax (at a reduced rate) in effect that year (table 1), and a short-lived provision that limited step-up in basis.

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 reinstated the estate and GST taxes for 2010 and extended them through 2012, with a $5 million estate tax exemption (indexed for inflation after 2011) and a top rate of 35 percent, but allowed executors to elect the EGTRRA rules for decedents who died in 2010. The 2012 rules were permanently extended by the American Taxpayer Relief Act of 2012, but the top rate was increased to 40 percent (table 1). The estate tax is effectively a flat-rate tax as explained below.

Here’s how the estate tax works:

- The executor must file a federal estate tax return within nine months of a person’s death if that person’s gross estate exceeds the exempt amount ($12.92 million in 2023).

- The estate tax applies to a decedent’s gross estate, which generally includes all the decedent’s assets, both financial (e.g., stocks, bonds, and mutual funds) and real (e.g., homes, land, and other tangible property). It also includes the decedent’s share of jointly owned assets and life insurance proceeds from policies owned by the decedent.

- The estate and gift taxes allow an unlimited deduction for transfers to a surviving spouse, to charity, and to support a minor child. Estates may also deduct debts, funeral expenses, legal and administrative fees, charitable bequests, and estate taxes paid to states. The taxable estate equals the gross estate less these deductions.

- A credit then effectively exempts a large portion of the estate: in 2023, the effective exemption is $12.92 million. Any value of the estate over $12.92 million is generally taxed at the top rate of 40 percent.

- The exemption level is portable between spouses, making the effective exemption for married couples double the exemption for singles. For example, if the first spouse to die bequeathed $5 million to children and grandchildren, the survivor’s exemption would increase by the unused $7.92 million.

- Although tax rates are graduated, all transfers in excess of the exemption are taxed at the top rate because the exemption far exceeds the $1 million threshold at which the top rate applies.

- Special provisions reduce the tax, or spread payments over time, for family-owned farms and closely held businesses. Estates that satisfy certain conditions may use a special-use formula to reduce the taxable value of their real estate, often by 40 to 70 percent. Family-owned businesses may often claim valuation discounts on the logic that when a business (including, potentially, one only passively investing in liquid assets) is divided among many heirs, the resultant minority stakes may have a market value less than proportional to the total value of the business. When farms or businesses make up at least 35 percent of a gross estate, the tax may be paid in installments over 14 years at reduced interest rates, with only interest due during the first five years.

- Inheritances are not taxable income to the recipient under the income tax.

- The basis for inherited assets is stepped up to the value at the time of death, meaning that unrealized capital gains on assets held until death are never subject to income tax. (Journalist Michael Kinsley famously called this the “angel of death loophole.”)

Here’s how the gift tax works:

- Congress enacted the gift tax in 1932 to prevent donors from avoiding the estate tax by transferring their wealth before they died.

- The tax provides a lifetime exemption of $12.92 million per donor in 2023. This exemption is the same that applies to the estate tax and is integrated with it (i.e., gifts reduce the exemption amount available for estate tax purposes). Beyond that exemption, donors pay gift tax at the estate tax rate of 40 percent.

- An additional amount each year is also disregarded for both the gift and estate taxes. This annual exclusion, $17,000 in 2023, is indexed for inflation in $1,000 increments and is granted separately for each recipient. Thus, a married couple with three children could give their children a total of $102,000 each year ($17,000 from each parent to each child) without owing tax or counting toward the lifetime exemption.

- Gifts received are not taxable income to the recipient.

And, here’s how the generation-skipping trust tax works:

- Congress enacted the GST tax in 1976 to prevent families from avoiding the estate tax for one or more generations by making gifts or bequests directly to grandchildren or great-grandchildren. The GST tax effectively imposes a second layer of tax (using the exemption and the top tax rate under the estate tax) on wealth transfers to recipients who are two or more generations younger than the donor.

Updated January 2024

Internal Revenue Code, 26 USC Subtitle B: Estate and Gift Taxes.

Joint Committee on Taxation. 2023. “Overview of the Federal Tax System as in Effect for 2023.” JCX-9R-23. Washington, DC.

Auxier, Richard. 2019. “The Death Tax Isn’t So Scary for States.” TaxVox (blog). Urban-Brookings Tax Policy Center. Washington, DC.

McClelland, Robert. 2019. “Fixing the TCJA: Restoring The Estate Tax’s Exemption Levels.” TaxVox (blog). Urban-Brookings Tax Policy Center. Washington, DC.

Gleckman, Howard. 2017. “Only 1,700 Estates Would Owe Estate Tax in 2018 under the TCJA.” TaxVox (blog). Urban-Brookings Tax Policy Center. Washington, DC.

Joint Committee on Taxation. 2015. “History, Present Law, and Analysis of the Federal Wealth Transfer System.” JCX-52-15. Washington, DC: Joint Committee on Taxation.

Harris, Benjamin. 2013. “Estate Taxes after ATRA.” Tax Notes. February 25.