Who pays the estate tax?

The top 10 percent of income earners pays more than 90 percent of the tax, with nearly 40 percent paid by the richest 0.1 percent. Few farms or family businesses pay the tax.

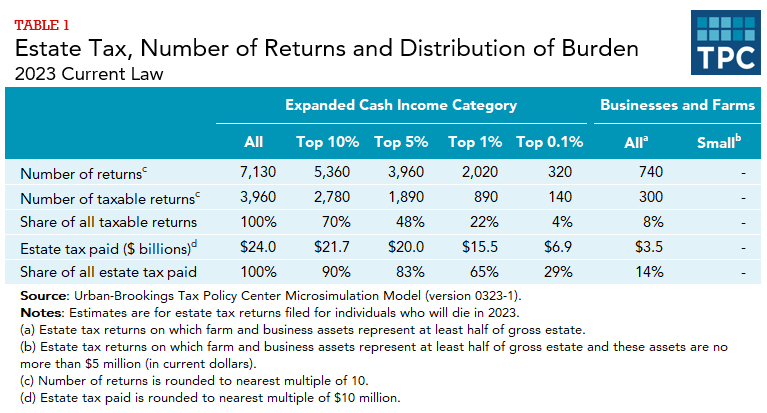

The Urban-Brookings Tax Policy Center (TPC) estimates that 7,130 individuals dying in 2023 will leave estates large enough to require filing an estate tax return.

Estates with a gross value under $12.92 million will not need to file this return in 2023. After allowing for deductions and credits, 3,960 estates will owe tax. TPC estimates that 70 percent of these 3,960 taxable estates will come from the top 10 percent of income earners and 22 percent will come from the top 1 percent alone (table 1).

Estate tax liability will total an estimated $24.0 billion in 2023. The top 10 percent of income earners will pay 90 percent of this total. The top 0.1 percent of earners will pay $6.9 billion, or 29 percent of the total (table 1).

According to TPC’s estimates, no small farm or small business – those with farm or business assets totaling no more than $5 million – will pay any estate tax in 2023. This is because of the $12.92 million effective exemption under the Tax Cuts and Jobs Act. The higher exemption amount, adjusted for inflation, expires after 2025, reverting to about half the amount.

Most estimates assume the decedent bears the estate tax, primarily because of data limitations. There is good reason to believe that heirs most often bear the tax in the form of lower inheritances. When the burdens are analyzed this way, individuals inheriting over $1 million are likely to bear most of the estate tax.

Updated January 2024

Urban-Brookings Tax Policy Center. “Microsimulation Model, version 0323-1.”

Batchelder, Lily. 2009. “What Should Society Expect from Heirs? The Case for a Comprehensive Inheritance Tax.” Tax Law Review 63 (1).

Batcheler, Lily 2020. “Leveling the Playing Field Between Inherited Income and Income From Work Through an Inheritance Tax.” In Emily Moss, Ryan Nunn, and Jay Shambaugh, editors. Tackling the Tax Code: Efficient and Equitable Ways to Raise Revenue. Washington, DC: Brookings Institution.

Harris, Benjamin. 2013. “Estate Taxes after ATRA.” Tax Notes. February 25. Washington, DC.

Joint Committee on Taxation. 2015. “History, Present Law, and Analysis of the Federal Wealth Transfer System.” JCX-52-15. Washington, DC.

Williams, Roberton. 2013. “Finally, a Permanent Estate Tax, Though Just for the Wealthy Few.” TaxVox (blog). Washington, DC: Urban-Brookings Tax Policy Center.