A health care flexible spending account is a tax-advantaged employer-sponsored account used to reimburse employees for qualifying health care expenses.

Health care flexible spending accounts (FSAs) are tax-advantaged benefit plans established by an employer to reimburse employees for qualified medical and dental expenses, such as copayments, deductibles, and prescription drug costs. FSAs are usually funded through salary-reduction agreements in which the employee agrees to receive lower monetary compensation in exchange for equivalent contributions to an FSA. For example, an employee who elects to reduce his or her monthly paycheck by $200 would receive, in return, a $2,400 annual contribution to his or her FSA.

The key benefit of FSAs is that these contributions are not subject to income or payroll taxes, which could mean significant tax savings for the account holder. An employee contributing $200 a month to an FSA would save $288 in federal income taxes if they were in the 12 percent tax bracket ($2,400 × 0.12 = $288) and an additional $184 dollars from reduced Social Security and Medicare payroll taxes ($2,400 × 0.0765 = $183.60). Because the federal income tax savings depend upon the employee’s income tax rate (which rises with income), the benefit of using an FSA is greater for higher-income workers. For example, the income tax savings for an employee in the 37 percent tax bracket with the same $2,400 annual contribution would be $888 ($2,400 × 0.37 = $888).

An important attribute of health FSAs is that employers must make the entire value of an employee’s FSA account available at the beginning of the year. For example, if either employee discussed above incurred a $3,000 medical expense in March, he or she could use the full $2,400 annual FSA contribution to help pay that cost, even though he or she would only have contributed $600 into the account.

In 2013, the Internal Revenue Service (IRS) instituted a contribution limit for health care FSAs. The limit is adjusted yearly for inflation; in 2023, it is $3,050 per year per employee. Generally, employees forfeit unused FSA funds at the end of the plan year, although employers may also offer one of two options:

- Provide a grace period of up to 2.5 months into a new plan year to use FSA money from the preceding plan year.

- Allow the employee to carry over up to a certain amount to use in the new plan year ($610 in 2023).

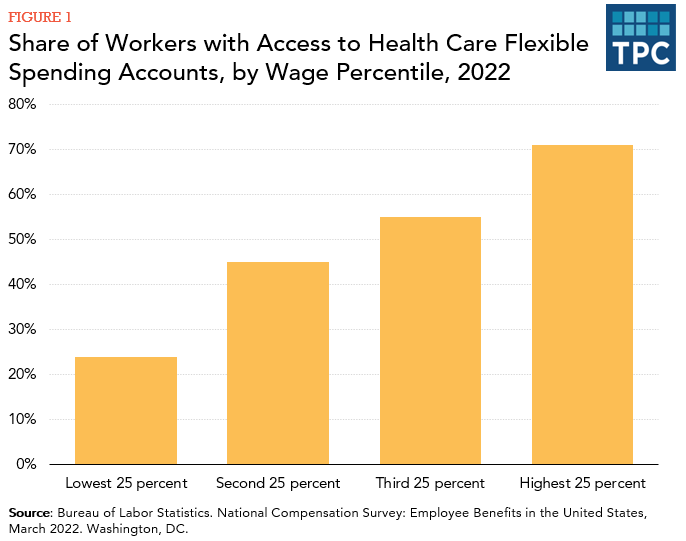

The Bureau of Labor Statistics in 2022 estimated that about 47 percent of all civilian workers had access to an FSA that year. High-income employees and employees in larger firms are more likely to have access. Nearly 1 in 4 low-income workers had access to an FSA in 2022 compared with around 7 in 10 workers at the top of the earning scale (figure 1).

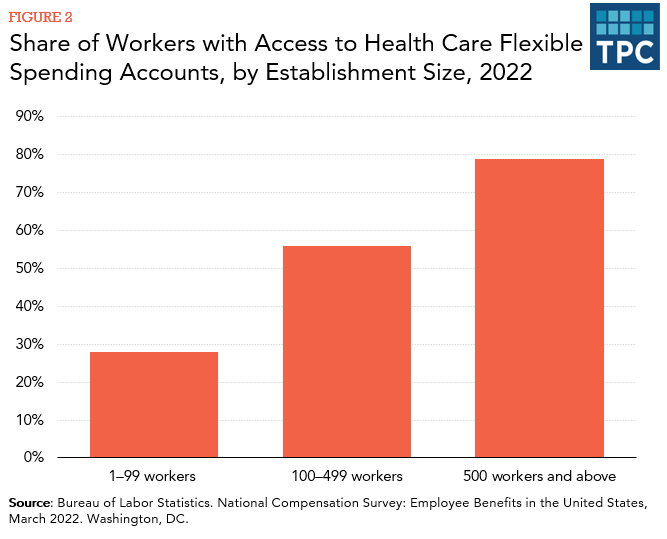

Employees in larger firms (500 or more workers) are more than twice as likely to have access than employees in smaller firms (99 or fewer workers), with 79 percent of the former reporting access versus 28 percent of the latter in 2022 (figure 2). Larger firms are typically better able to handle the complexity and administrative costs of offering FSAs.

More specific data on exactly who uses FSAs and how much federal tax revenue they cost are difficult to obtain because employees are not required to report FSA elections on federal income tax returns, and few surveys ask specifically about FSA participation.

Updated January 2024

Internal Revenue Service. 2013. “Application of Market Reform and Other Provisions of the Affordable Care Act to HRAs, Health FSAs, and Certain Other Employer Healthcare Arrangements.” Notice 2013-54. Washington, DC.

Internal Revenue Service.2022. “Revenue Procedure 2022-38.” Washington, DC.

Internal Revenue Service. 2017. “Medical and Dental Expenses (Including the Health Coverage Tax Credit) for Use in Preparing 2017 Returns.” Publication 502. Washington, DC.

Joint Committee on Taxation. 2008. “Tax Expenditures for Health Care.” JCX-66-08. Washington, DC.

Rapaport, Carol. 2013. “Tax-Advantaged Accounts for Health Care Expenses: Side-by-Side Comparison, 2013.” Washington, DC: Congressional Research Service.