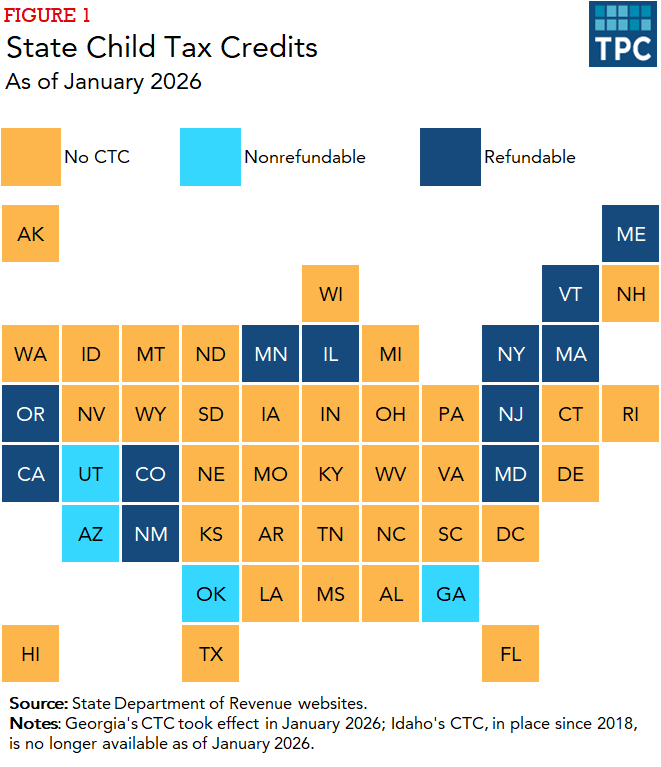

The federal child tax credit (CTC), provides a partially refundable tax credit to households with eligible children. As of January 2026, 16 states additionally offered a state CTC. Both the amount of the credit and the eligibility rules for households vary considerably across states.

As of January 2026, 16 states offered a state CTC. Among these states, 12 offered a refundable CTC (if the credit exceeds a filer’s state income tax liability, then the filer receives the excess amount as a payment), and four offered a nonrefundable CTC (the credit can only be used to reduce the filer’s tax liability).

Notably, 14 of these state CTCs were either enacted or expanded since 2021, when Congress temporarily expanded the federal CTC as part of the American Rescue Plan Act. Georgia passed legislation to create its new nonrefundable CTC in May 2025, taking effect in January 2026. In March 2026, Utah increased the income phase-out threshold for its nonrefundable CTC for tax year 2026. Idaho’s CTC, in place since 2018, sunset as of January 2026 and is no longer available. In June 2026, New Jersey passed an expansion to its refundable CTC, increasing its maximum credit amount from $1,000 to $1,250 per qualifying child for tax year 2026. Additionally, in June 2026, Rhode Island passed a new CTC that will take effect in January 2027 and provide $330 per child under 19 in eligible households.

This count of state CTCs does not include related policies in states, including personal credits for all eligible members of a household (e.g., Arkansas’s $29 personal credit functions similar to a personal exemption) or per child tax deductions (e.g., North Carolina, which changed its child tax credit to a deduction in tax year 2018). Instead, these 16 states specifically offer a tax credit for children in addition to their state personal exemption or a relatively large state standard deduction.

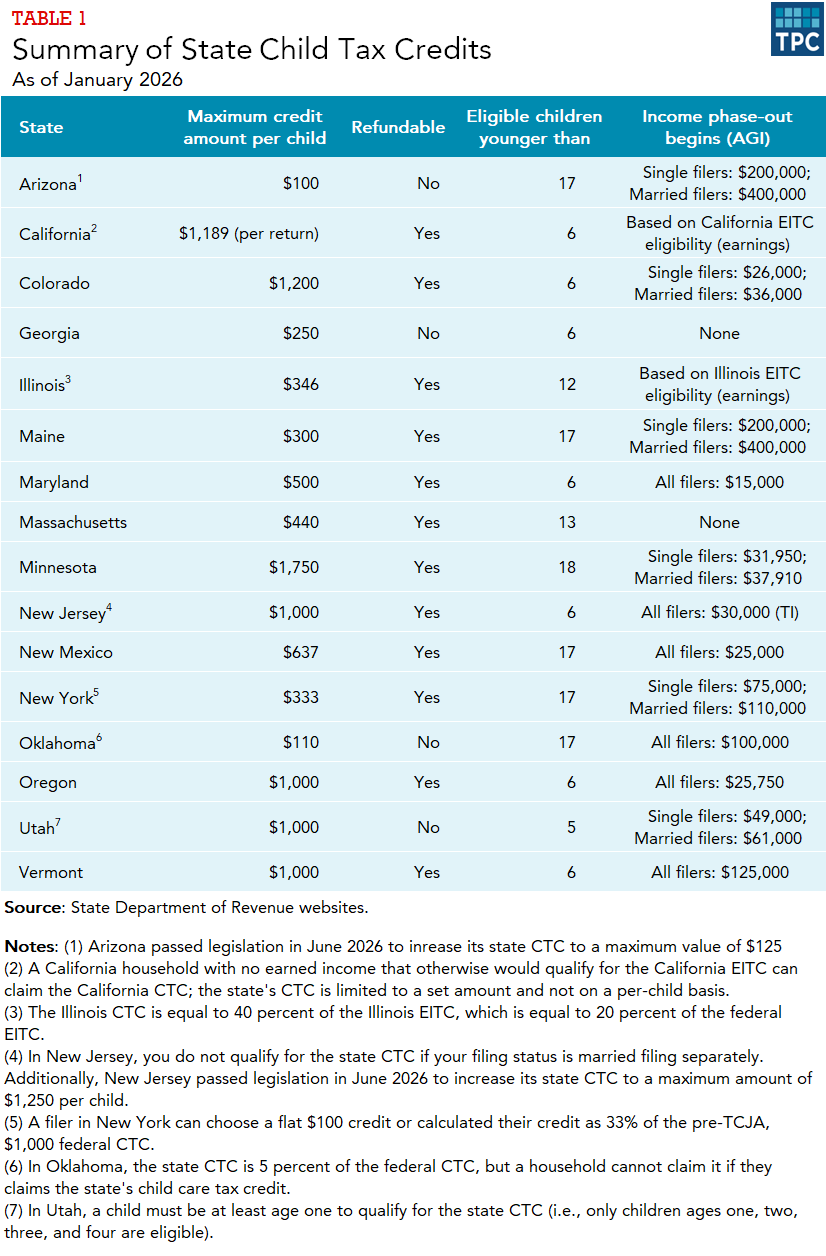

Unlike the state earned income tax credit (EITC), which is generally calculated as a share of the federal credit, state CTCs are often calculated independent of the federal CTC. State policymakers have varied the amount of the credit, age eligibility rules for children, income limitations for the filer, and whether or not the credit is fully refundable, meaning that families can receive the maximum benefit without having earnings.

As of January 2026, state CTC amounts per eligible child ranged from $100 in Arizona to $1,750 in Minnesota (see Table 1). In total, six of the 16 states provided a credit amount of $1,000 or more per child. Most states provided their CTC as a flat amount, but New York and Oklahoma calculated their credit as a percentage of the federal CTC for 2025. And every state but one provided a credit for each eligible child on their tax return—California, the exception, provided a single credit to an eligible household.

The federal CTC is available to filers with eligible children younger than age 17, and six states used the same age cutoff for their state CTC. Seven states limited their credit to children younger than age 6. Limiting the credit to younger children is a way for states to provide relatively large tax benefits to fewer households. Young children are often specifically targeted because evidence shows that a child’s early years are crucial to their development.

Other than Georgia, Idaho and Massachusetts, all states prevented households with federal adjusted gross income (AGI) above a certain threshold from claiming their state CTC. The income thresholds at which point a filer began to lose their CTC varied widely across states: Maryland limited its credit to households with less than $15,000, regardless of filing status, while Maine and Arizona both began to phase out their credits at $200,000 for a single filer and $400,000 for a married couple. Most states phased out their CTC over a range of income. For example, a Vermont household's credit was reduced by $20 for every additional $1,000 in income above the $125,000 threshold (for all filers) until the credit was completely eliminated. Thus, Vermont has a 2 percent phaseout rate. The federal CTC phaseout rate is 5 percent.

Twelve state child tax credits were refundable and four were nonrefundable as of January 2026. If a refundable tax credit exceeds a household’s state income tax liability, the household receives the excess amount as a state tax refund. In contrast, a nonrefundable credit can only offset a taxpayer’s state income tax liability. One important difference between most state refundable CTCs and the federal refundable CTC is that all 12 refundable state credits are “fully refundable.” That is, a household in these states with an eligible child gets the full CTC even if they have little or no income. In contrast, a taxpayer must earn $2,500 before they can begin to qualify for the federal CTC and after that, the benefit begins to phase in. Some families with low incomes in states with a fully refundable CTC will receive a state CTC but no federal CTC.

Updated July 2026

Urban-Brookings Tax Policy Center. 2025. What is the Child Tax Credit?. Tax Policy Center Briefing Book. Washington, DC.

Boddupalli, Aravind, Luisa Godinez-Puig, Gabriella Garriga, and Harley Webley. 2025. Helping Maryland Connect Underserved Residents to Crucial State Tax Credits. Washington, DC: Urban Institute.

Maag, Elaine, and Peter Subkoviak. 2024. Learning from Federal Experience, Minnesota Will Soon Advance State-Level Child Tax Credit Payments. TaxVox (blog). Washington, DC: Urban-Brookings Tax Policy Center.

Airi, Nikhita, and Richard Auxier. 2024. Three Lessons for Policymakers Designing a State Child Tax Credit. TaxVox (blog). Washington, DC: Urban-Brookings Tax Policy Center.

Auxier, Richard, David Weiner, and Nikhita Airi. 2024. Constructing a Child Tax Credit That Fits Every State. Washington, DC: Urban-Brookings Tax Policy Center.

Auxier, Richard and David Weiner. 2023. Who Benefited from 2022's Many State Tax Cuts and What is in Store for 2023?. Washington, DC: Urban-Brookings Tax Policy Center.

Maag, Elaine and David Weiner. 2021. How Increasing the Federal EITC and CTC Could Affect State Taxes. Washington, DC: Urban-Brookings Tax Policy Center.