The Affordable Care Act provides families with refundable, advanceable tax credits to purchase health insurance through exchanges. Premium credits cap contributions as a share of income for families with incomes over 100 percent of the federal poverty. After 2025, the credit will be less generous and only be available to families with incomes below 400 percent of FPL.

ACA Tax Credits for Health Insurance

The Affordable Care Act (ACA) provides families with refundable tax credits to purchase health insurance through both state and federal Marketplaces. Tax filers can claim premium credits if they (1) have incomes over 100 of the federal poverty level (FPL), (2) are ineligible for adequate and affordable health insurance from other sources, and (3) are legal residents of the United States. Tax filers with incomes between 100 and 138 percent of the FPL are generally ineligible for premium credits if they reside in states that take advantage of the ACA’s Medicaid-eligibility expansion. After 2025, enhancements made by the American Rescue Plan Act of 2021 and extended by the Inflation Reduction Act of 2022 will expire, as the One Big Beautiful Bill Act (OBBBA), or 2025 reconciliation act, did not extend the enhancements. Premium credits will be less generous and only be available to families with incomes below 400 percent of FPL.

Additionally, the OBBBA and new federal rules published in 2025 added new restrictions that will likely reduce the number of families claiming the premium tax credit. Restrictions include taking away eligibility for many lawfully present immigrants, limiting passive reenrollment through stricter verification of eligibility, and eliminating special enrollment periods for families with incomes below 150 percent of the federal poverty level.

Calculation of Premium Credits

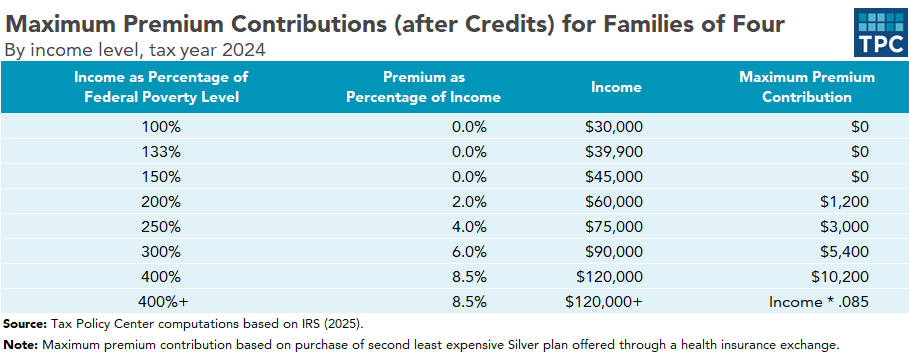

Premium credits effectively cap family contributions as a share of income for those purchasing midrange “benchmark” plans. In 2024, families with incomes at or below 150 percent of FPL pay nothing for a benchmark plan. For families with higher incomes, maximum family contributions range from a nominal contribution for families with income at 151 percent of FPL to 8.5 percent of income for families at 400 percent of FPL and higher (table 1). Premium credits equal the difference between gross premiums and maximum family contributions.

For example, consider a family of four with income equal to 200 percent of FPL in 2024 purchasing an insurance plan costing $15,000. Multiplying family income (here, $60,000) by the applicable 2.0 percent maximum premium results in a family contribution of $1,200 and thus a premium credit of $13,800 ($15,000- $1,200).

The example above assumes family purchases the second least expensive (Silver) plan from the menu of Bronze, Silver, Gold, and Platinum health insurance plans offered through Marketplaces. If the family purchased a more expensive plan, the credit would remain the same and the family would pay the full difference in premiums.

Advance Premium Credits and Reconciliation

Premium credits are based on a household’s income in the tax year premiums are paid. The credits are calculated the following year, when households file their income tax returns. However, the Treasury usually sends advance payment of premium credits directly to the insurance company, and the household pays a reduced premium. The advance payment of credits is based on estimated income, generally from the last tax return filed before enrollment in health insurance. If actual income in the year of enrollment is less than estimated income, families qualify for additional credit amounts when filing their returns. If actual income is greater than estimated income, families must repay the difference between the advance credit and credit amount at filing, per OBBBA provisions. This could present significant hardships for families with limited savings.

Prior to OBBBA, for most households with large income increases, the maximum reconciliation payment was limited. In tax year 2024, the maximum payment ranged from $750 for married couples with incomes below 200 percent of FPL to $3,150 for couples with incomes of at least 300 but less than 400 percent of FPL (table 2). Families whose income equals 400 percent or more of FPL had no limit on reconciliation payments.

Updated October 2025

Burman, Leonard E., Gordon B. Mermin, and Elena Ramirez. 2015. “Tax Refunds and Affordable Care Act Reconciliation.” Washington, DC: Urban-Brookings Tax Policy Center.

Internal Revenue Service. 2025. “2024 Instructions for Form 8962: Premium Tax Credit (PTC).” Washington, DC.

Jacobs, Ken, Dave Graham-Squire, Elise Gould, and Dylan Roby. 2013. “Large Repayments of Premium Subsidies May Be Owed to the IRS If Family Income Changes Are Not Promptly Reported.” Health Affairs 32 (9): 1538–45.