Tax expenditures are revenue losses that occur when federal tax law provisions reduce what individuals or businesses owe in taxes. They support certain activities, or they assist specific groups of taxpayers. They can be politically attractive, since they help advance policy goals without increasing the visible size of government —you can’t “see” revenue that was never collected. But they still have a significant fiscal impact: They reduce revenue that would otherwise have been collected.

Understanding the types of tax expenditures and who benefits from them can offer valuable insight into policy priorities and help identify opportunities to improve tax policy.

Types of tax expenditures

- Exclusions are income amounts not counted in taxable income. An example is the value of employer-provided health insurance. Since federal individual income tax rates are calculated based on your taxable income, exclusions can lower total tax liability.

- Itemized deductions like those for mortgage interest or charitable contributions, are available only to taxpayers whose total value of deductions exceeds the value of the standard deduction. Since the 2017 Tax Cuts and Jobs Act increased the standard deduction, fewer taxpayers—about 10 percent in 2025—are expected to itemize, most of them relatively high income.

- Credits reduce tax liability directly. Most tax credits are nonrefundable; that is, they can only reduce a filer’s tax liability to zero; filers cannot receive any more. Some, however, like the child tax credit (CTC), allow taxpayers to receive a some of the credit if the value of the credit is greater than their tax liability. Others, like the earned income tax credit (EITC) and the premium tax credit, are fully refundable, meaning taxpayers can keep the entire credit amount if its value is greater than what they owe.

- Preferential rates apply to specific types of income, such as long-term capital gains and qualified dividends, which are taxed at lower rates than ordinary income.

- Deferrals allow taxpayers to postpone tax payments. They include retirement savings contributions and accelerated depreciation of business investments.

Not every deduction or exclusion is a tax expenditure. Deductions that reflect true business costs (like employee wages or loan interest) are not considered tax expenditures. And the standard deduction, which exempts a basic level of income from tax and is treated as part of the tax system’s baseline, is not considered a tax expenditure.

Who benefits from tax expenditures

- The exclusion for employer-provided health insurance delivers about 45 percent of its total benefit to the top quintile of earners, and just over 1 percent of its benefit to the bottom quintile.

- The deduction for home mortgage interest and real estate taxes is more concentrated among higher-income households, with nearly 75 percent of the benefit going to the top 20 percent of earners, while the bottom 60 percent receive just under 8 percent.

- The deduction of state and local taxes is also concentrated among higher-income households, with about 70 percent of its benefit going to the top quintile, and about 30 percent of the benefit going to the bottom 60 percent.

- The child tax credit benefits most income groups proportionately, with the top four quintiles each receiving between 20 and 25 percent of the benefit.

- The earned income tax credit (EITC) sees 90 percent of its benefit going to the bottom 40 percent of households (by design, none go to the top quintile).

- More examples are here.

Tax expenditures can be costly

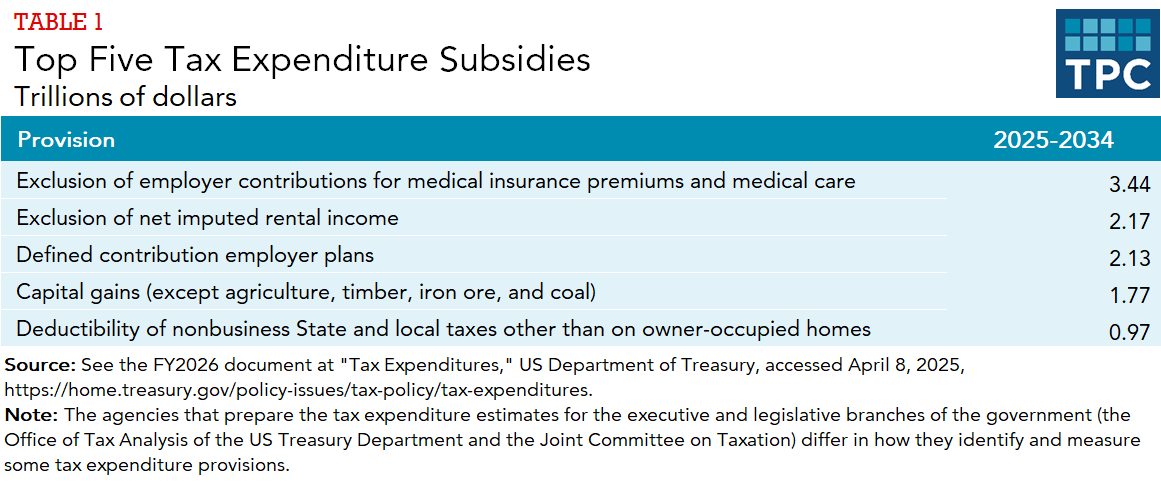

Table 1 presents the estimated revenue cost of the five most costly tax expenditures from 2025-2034. Together they are projected to incur $10 trillion over that period.

Understanding tax expenditures is key to evaluating both equity and efficiency in federal tax policy. Though often hidden in the tax code, their scale can rival major spending programs. Their distribution tells us who benefits from them.

Learn more:

TPC Briefing Book: Tax Expenditures

Video: What are tax expenditures?

Video: Are tax expenditures a problem?

TaxVox Blog: A bigger, easier target for DOGE: Tax Expenditures

Research Report: Are Tax Expenditures Worth The Money?