Business income is generally taxed in one of two ways. Corporate profits can be taxed at the entity level and then again when earnings are distributed to shareholders. In contrast, pass-throughs businesses – such as sole proprietorships, S-corps, and partnerships – do not pay tax at the entity level, but rather earnings are “passed through” to business owners. Owners declare and pay taxes on those earnings on their individual income tax returns.

The 2017 Tax Cuts and Jobs Act (TCJA) reduced taxes for both corporations and pass-throughs. While the corporate tax rate fell from 35 percent to 21 percent, many pass-through businesses became eligible for a 20 percent income tax deduction. The deduction effectively reduces the top individual tax rate on qualifying income from 37 percent to 29.6 percent.

At the time, advocates of the pass-through tax break argued it would help small businesses and ensure similar tax reductions for pass-throughs and corporations. However, tax experts argued the tax break favored wealthier taxpayers, failed to stimulate the economy, and created inequities between individuals who earned business income and individuals who relied on ordinary income such as wages.

Many provisions in the TCJA, including the pass-through deduction, are scheduled to expire at the end of 2025. Republicans in Congress are looking to make the deduction permanent and more generous. As this debate continues, the latest TPC tax model estimates show which filers are benefiting from the deduction.

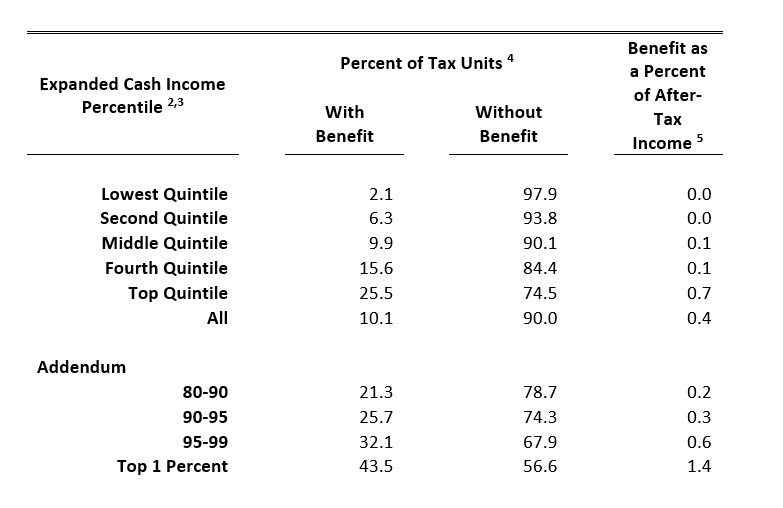

In calendar year 2025, TPC estimates that about 10 percent of middle-income households (those making between $65,800 and $117,000) will claim the pass-through deduction. Among households in the top 1 percent of earners (those making at least $1.1 million), 43.5 percent will claim the tax break.

Higher-income households will also receive larger benefits from the deduction. For the top 1 percent, the deduction will increase their average after-tax income by 1.4 percent (about $32,000). The average change in after-tax income from the pass-through deduction for households in the middle and fourth quintile will be 0.1 percent ($60 and $170 respectively).