A bipartisan tax plan that overwhelmingly passed in the House is now stuck in the Senate in part because of proposed changes to the child tax credit (CTC). While proponents argue the bill would deliver benefits to the families who need them the most, critics are concerned a more generous CTC could negatively affect incentives to work.

As Congress debates the policy, it’s worth noting there are places where a more generous CTC that benefits families with very low income is not just a theoretical debate: the states.

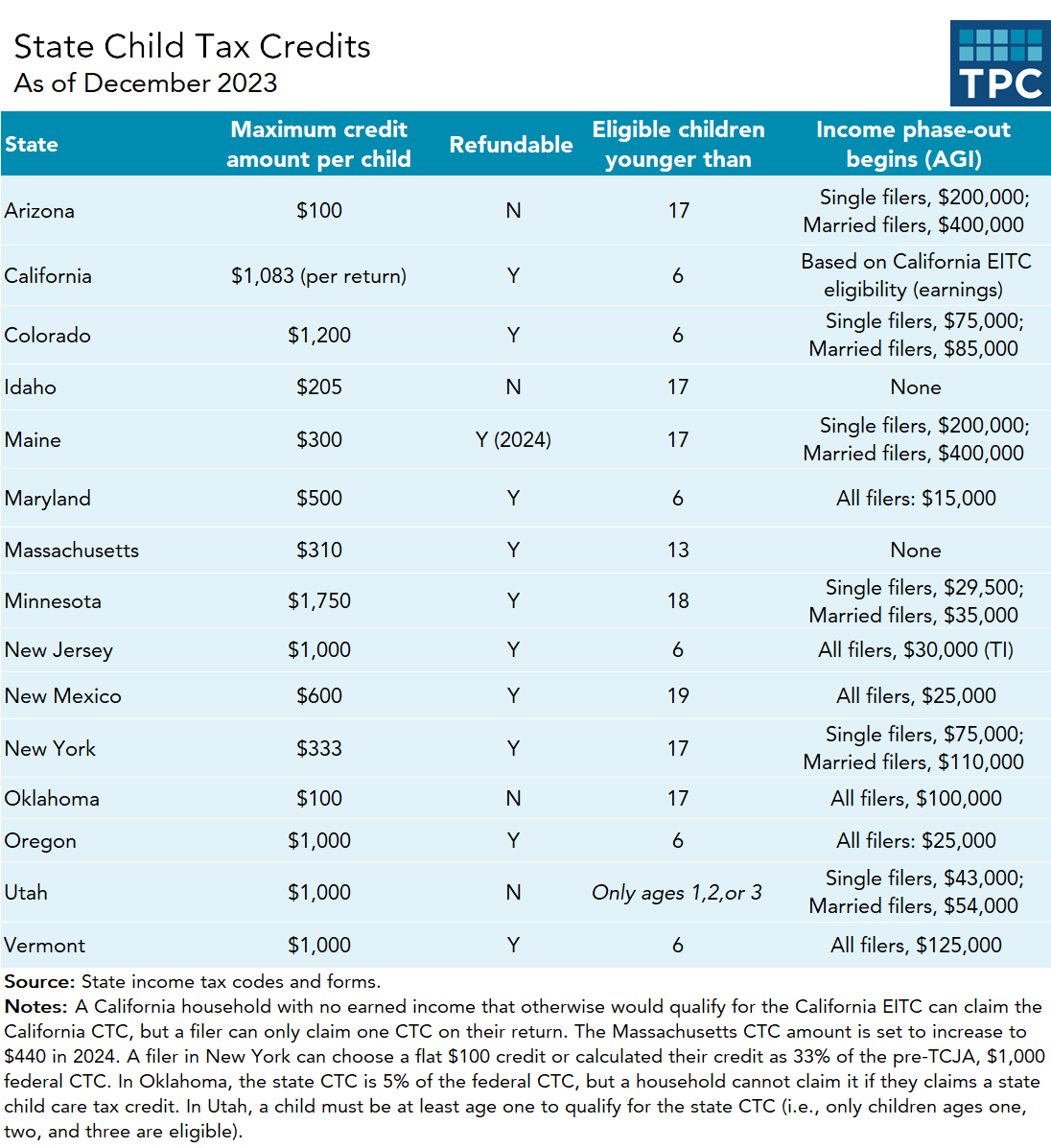

As explained in a new brief on state child tax credits, 11 states currently provide a “fully refundable” CTC. That is, there is no income phase in, so a family with an eligible child but little or no income still gets the state credit. And if the refundable state credit exceeds the household’s state income tax liability, the household receives the excess amount as a refund payment from the state.

That is not the case with the federal credit. The current version of the federal CTC requires a household to have earned income of at least $2,500 before it can see any benefit from the federal CTC, and it must earn roughly $25,000 to get the full refundable CTC.

Further, while the federal CTC provides a $2,000 credit per eligible child, the refundable portion of the credit is capped at $1,600 for the entire households—regardless of how many eligible children are in the family.

As a result, there are some families in these 11 states benefiting from the state CTC but not the federal CTC.

And many of these fully refundable state child tax credits are nearly as large as the refundable portion of the federal CTC. Colorado, Minnesota, New Jersey, Oregon, and Vermont all offer a maximum per child credit of $1,000 or more. California also offers a refundable CTC greater than $1,000, but its amount is per tax return and not per child.

That said, there are often other limitations on these state credits. Specifically, the state credits in California, Colorado, New Jersey, Oregon, and Vermont are restricted to families with children younger than age 6. In contrast, the federal CTC is available to children younger than age 17. States often limit child tax credits to younger children so they can deliver a relatively large benefit to eligible families but at a lower total annual revenue cost.

And, in another attempt to limit the cost of the credit, all of these states start to phase their CTC benefit out at a lower level of income than the federal CTC. For example, the Minnesota CTC begins to phase out after a single parent’s income exceeds $29,500, while a single parent gets the full benefit of the federal CTC until her income exceeds $200,000.

Most of these credits were enacted a year or two ago, so there does not yet exist the same research track record on how state credits affect parents’ decisions to work

But if Congress wants more evidence about the tradeoffs involved in constructing a more generous child tax credit, state CTCs are a great place to learn.

And that would only be fair given that Congress first inspired states to enact child tax credits. Of the 15 existing state child tax credits, 12 were either enacted or expanded after the American Rescue Plan significantly but temporarily expanded the federal CTC.