Scrambling for a politically acceptable way to raise revenue to pay for a scaled-down social spending and climate bill, Senate Democrats are considering a plan to expand the Net Investment Income Tax (NIIT). Predictably, critics allege the plan would hurt small, family business.

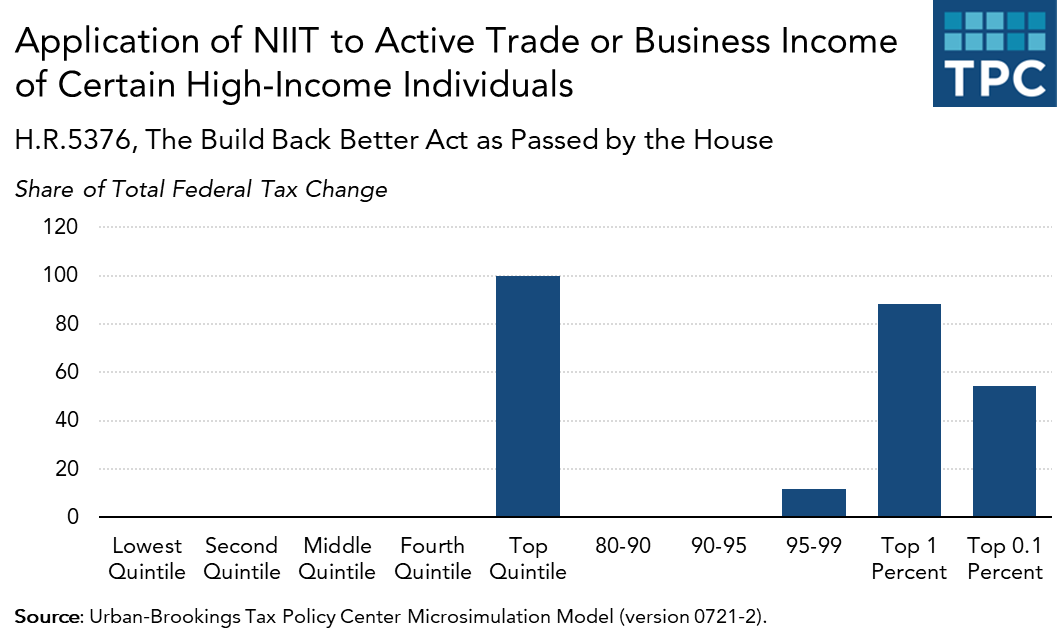

But a new Tax Policy Center analysis finds that in 2023 the burden of the House version of this tax hike overwhelmingly would fall on the highest income 1 percent of households (those making $885,000 or more). More than half the new tax would be paid by the top 0.1 percent, those making $4 million or more. Households making $1 million or more would pay about 85 percent of the expanded tax.

Who pays, and who doesn’t

The 3.8 percent NIIT was included in the 2010 Affordable Care Act (ACA). It applies only to unmarried filers making $200,000 or more or joint filers making $250,000 or more. The tax is imposed on investment income such as interest, dividends, capital gains, rents and royalties, and, crucially, business income that the tax code treats as passive, as opposed to active.

While many owners of pass-through businesses must pay the NIIT under current law, others do not. For example, active owners of S Corporations generally are exempt from the tax. There were more than 4.7 million of these businesses in 2017.

Similarly, real estate professionals do not have to pay the NIIT on rental income.

Two big changes

The House bill would make two big changes. First, for high-income households, it would expand the tax to include all business income, whether or not the taxpayer materially participates in the business, as long as that income is not already subject to payroll taxes. In effect, S Corporation shareholders, limited partners, and other owners of pass-through business who now are exempt would get hit by the NIIT.

Second, solely for that active income, the House bill would raise the income threshold to $400,000 ($500,000 for couples filing jointly). That would require two separate income thresholds, a feature that exclude the vast majority of business owners but also would make filing more complex (though those affected are likely to have accountants doing the work).

High-income payers

Nearly 99 percent of households would be entirely exempt from the new tax simply because they fall below that $400,000 threshold. TPC estimates that about 88 percent of the expanded NIIT would be paid by the top 1 percent. About 54 percent would be paid by those in the top 0.1 percent.

The rest, about 12 percent, would be paid by those making between about $372,000 and $885,000 (those between the 95th and 99th income percentiles).

The trade group S Corp.org charged, “Expanding the NIIT would raise taxes on small and family-owned businesses.” Family-owned? Often. Small? Not necessarily. In 2005, 0.3 percent of S Corporations with at least $50 million in annual income accounted for one-quarter of all income for these firms, according to my TPC colleague Donald Marron.

Effects on small businesses

Of course, we could argue endlessly about what a small business is. But we probably could agree that someone with annual modified adjusted gross income of $1 million or more is not a struggling entrepreneur.

We know that about 14 percent of tax filers reported some business income on their federal income tax returns, but only about 5.5 reported business income that accounted for at least half of their adjusted gross income. On average, business owners report only about $32,000 in business income. They will not need to spend time worrying about the NIIT expansion.

We also know that about 85 percent of partnership and S Corporation income was earned by households making $200,000 or more, and half was made by households with $1 million or more in annual income. They may need to check with their accountants.

It remains to be seen whether Congress will finally agree to any expansion of the NIIT. But if it does, the vast majority of family-owned small business will be entirely unaffected.