In his 2024 campaign, President Trump proposed cutting the corporate tax rate to 15 percent for companies that manufacture in the US. Now, the reconciliation bill moving through Congress proposes to achieve the same goal. But rather than cutting the corporate rate, the bill changes how the tax code treats investments in new manufacturing plants.

If passed, it would offer immediate savings to firms that build in the US, which could spur billions of dollars in new investment. But because the proposed measure is temporary, higher investment in the short-term may simply reflect a shifting from future investment to take advantage of the policy. And design and enforcement will be key elements in its success.

A shift from rate cuts to “full expensing”

The House GOP plan would allow firms to fully and immediately deduct the cost of building new manufacturing, production, or refining facilities. This “full expensing” would apply to construction starting between January 19, 2025, and January 1, 2030, with new property placed in service before 2033. (This is distinct from the reconciliation bill’s extending “bonus depreciation” that had already started to phase out under the 2017 Tax Cuts and Jobs Act.)

The provision is estimated to cost about $30 billion a year until 2029 and $150 billion over a decade.

Under current law, a business recovers the cost of a new building gradually, typically over 39 years, using depreciation. For example, a $100 million plant allows a company to deduct only about $2.5 million annually. But under full expensing, a company could deduct the entire cost of a new facility in the year construction begins, significantly improving near-term cash flow.

Compared to a lower corporate tax rate, which would benefit all profits, immediate full expensing specifically targets new investments. This improves business cash flow and reduces the cost of building new manufacturing capacity.

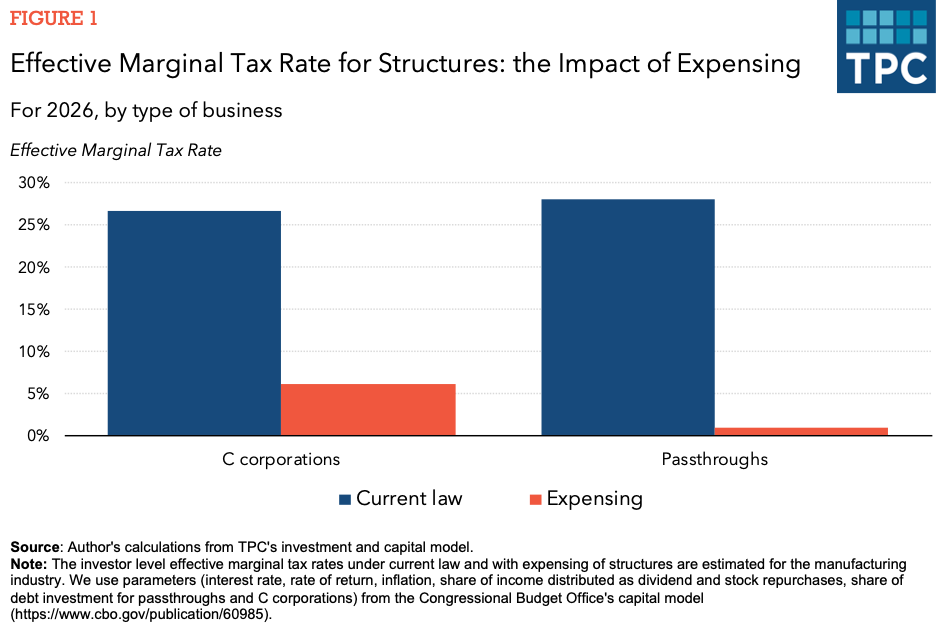

Quantifying the investment incentive

To measure the potential impact of expensing structures on the effective taxation of marginal investments, I used TPC’s Investment and Capital Model to calculate effective marginal tax rates (EMTRs) on eligible buildings. EMTRs measure the burden of taxes on marginal investment—in other words, investments that just break even. Businesses seek low EMTRs because they reflect a lower cost of investing.

Under current law, C corporations face an average EMTR of 27 percent for structures, while pass-through entities face 28 percent. Full expensing would substantially reduce these rates to 6 percent and below 1 percent, respectively. The user cost of capital, or the minimum rate of return for profitable investment, would decrease by about 20 percent.

Estimates vary widely on investment's responsiveness to changes in the user cost of capital. For example, the Congressional Budget Office estimates that when the user cost of capital decreases by 1 percent, investment goes up by 0.7 percent—within the 0.5 to 1 percent range reported by many studies.

A projected 20 percent decrease in the user cost of capital from expensing structures would therefore increase investment by 14 percent. But other recent studies have found a larger response. However, since Congress has never allowed expensing of structures, and very few countries around the world allow it, there’s some uncertainty about how firms might respond.

How much of the economy would qualify?

In 2024, real private investment in non-residential structures was over $900 billion, with about $230 billion—roughly 26 percent—coming from the manufacturing sector alone.

The House bill covers more than manufacturing. Expensing would also be allowed for chemical and agricultural production, and refining operations like fuel processing. The proposal would exclude non-production uses such as offices, parking structures.

Expensing’s success would depend on execution

Broad-based expensing is a simple and effective way to lower the cost of building manufacturing facilities in the US. But the House bill provision’s restriction to certain industries and specific uses could introduce new complexities that the IRS would need to address through additional regulations.

For example, the new provision would be restricted to areas of new buildings used for production. This would require more documentation than full expensing of all structures – in addition to detailed IRS guidance and meticulous business recordkeeping to define and track qualifying income.

Expensing a 39-year investment also creates tax avoidance opportunities: The IRS will have to clarify and enforce transfer and recapture rules.

And while lowering the cost of building new production facilities and increasing cashflow could boost investment, only firms with enough taxable income would be able to fully take advantage of it. Encouraging domestic investment in low-profit industries or by businesses with low taxable income may require more targeted policies.