Mistakes happen during tax filing season, so Congress has given the IRS “math error authority” to correct some of them. If the agency corrects a perceived error on a tax return under math error authority, they notify taxpayers with “math error notices.”

The “Internal Revenue Service Math and Taxpayer Help Act,” or IRS MATH Act, aims to improve those notices. Co-sponsored by Sens. Elizabeth Warren (D-MA) and Bill Cassidy (R-LA) and Reps. Randy Feenstra (R-IA) and Brad Schneider (D-IL), the bill would require the IRS to use “comprehensive plain language” in math error notices, and explain how IRS corrections affect any taxes owed or refund amount.

That's good news: Simplifying and clarifying the way the IRS communicates with taxpayers upon discovery and correction of potential tax return errors improves tax administration and compliance. But Congress should heed the advice of the National Taxpayer Advocate and be judicious in expanding IRS math error authority or risk further burdening taxpayers.

Why are math error notices under scrutiny right now?

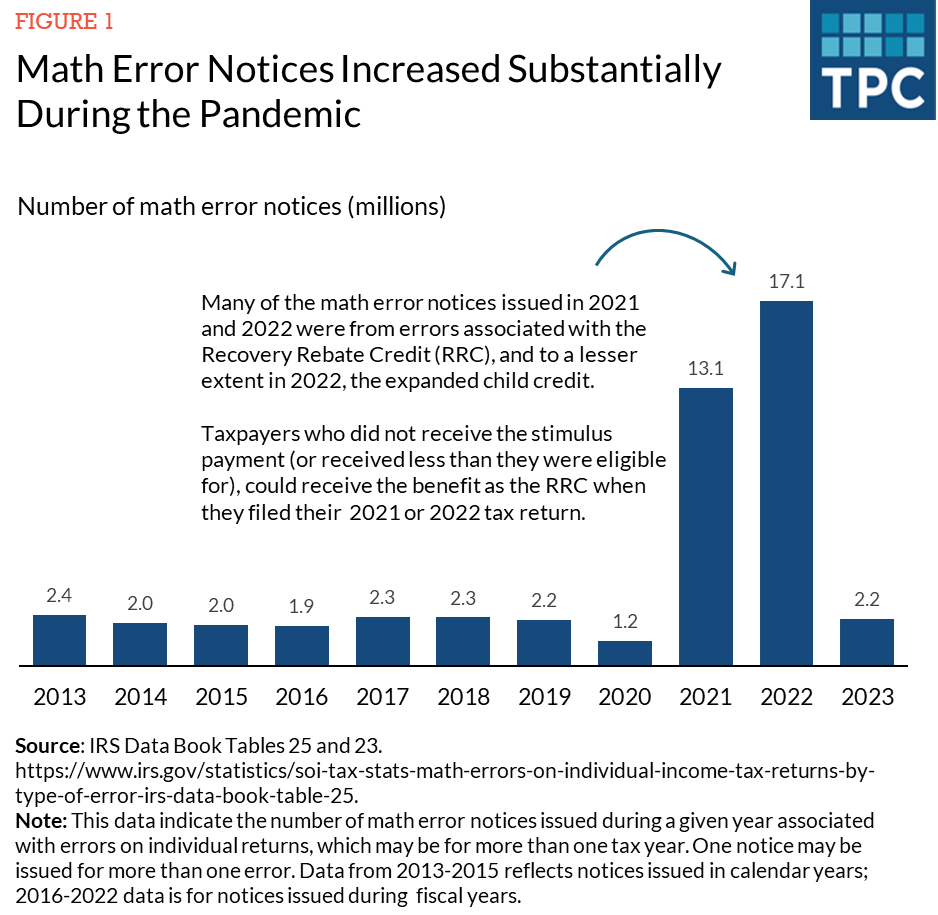

One reason for the current scrutiny of math error notices may be the sheer volume of them recently, as illustrated in Figure 1. Most were associated with now-expired pandemic-era programs.

For example, if a taxpayer had not received the portion of an Economic Impact Payment (i.e., “stimulus check”) associated with their child, they could have claimed the additional amount as the recovery rebate credit (RRC) on their return.

But, if they failed to provide the child’s Social Security number (SSN) or transposed a digit in the SSN, Congress provided the IRS with math error authority to recompute their credit amount. The IRS would then send the taxpayer a math error notice which, as the National Taxpayer Advocate documents, would include language like:

“We changed the amount claimed as Recovery Rebate Credit on your tax return. The error was in one or more of the following:

- The Social Security number of one or more individuals claimed as a qualifying dependent was missing or incomplete.

- The last name of one or more individuals claimed as a qualifying dependent does not match our records.

- One or more individuals claimed as a qualifying dependent exceeds the age limit.

- Your adjusted gross income exceeds $75,000 ($150,000 if married filing jointly, $112,500 if head of household).

- The amount was computed incorrectly.”

It’s easy to understand why taxpayers were confused. Offered five possible reasons for a mistake, a taxpayer had little way of knowing which mistake they had made. Worse yet: Many letters failed to note taxpayers had 60 days to respond. (The IRS later corrected that omission.)

The pandemic may have exposed more taxpayers to “vague and confusing” math error notices, but the National Taxpayer Advocate has for years cited the “lack of clarity” of math error notices. This lack of clarity can be particularly burdensome on lower-income and vulnerable taxpayers. For example, populations with limited English skills or computer access, or with lower literacy rates or education levels, may struggle to understand their mistake or wonder how to respond if they disagree with the IRS’s determination.

In addition to explaining math errors in plain language, the IRS MATH Act would require the IRS to specify which line of the tax return contains the error and provide an itemized computation of all the changes made to the return upon correcting the error. The IRS would no longer be allowed to provide lists of multiple issues that may have triggered a math error.

Why does the IRS use math error authority at all? Don’t IRS audits catch mistakes?

Math error is one tool the IRS has to administer and ensure compliance with the tax code, but it often gets less attention than the more common IRS tool—the audit. However, while audits can be burdensome—and many taxpayers may not even reply to an audit notice—they can provide more legal protections and options for recourse than math error.

In an audit, if the IRS detects a potential error, they issue an initial notice to the taxpayer explaining what they believe to be the error and their proposed change. The taxpayer has 30 days to respond to the initial notice, either agreeing with or appealing the decision. If the taxpayer’s initial appeal is unsuccessful or if the taxpayer does not respond to the 30-day notice, the IRS issues a notice of deficiency. The taxpayer has another 90 days to respond, which could mean taking the issue to US Tax Court.

Congress gave the IRS math error authority so the agency could quickly correct certain errors on a tax return, usually before a refund is issued, without needing additional information from the taxpayer. The IRS often detects these potential errors either because the error is obvious (like a computational error, number transposition, or omission of required information) or because of a discrepancy between information on the return and other government databases.

With math error authority, the IRS can correct the perceived error and recalculate any taxes owed or the refund amount and send a math error notice alerting the taxpayer to the correction. That notice must “set forth the error alleged and an explanation thereof.”

The taxpayer has 60 days to “request an abatement,” or disagree with the adjustment in writing, over the phone, or in person.

Unlike an audit, absent a taxpayer response to the initial notice, the adjustment stands, leaving the taxpayer with limited remaining legal options.

IRS math error authority works when mistakes are easy to verify accurately.

Math error authority can be an appropriate compliance tool when errors are clear, verifiable with accurate government information, or quickly corrected without evaluation of additional documentation. For example, the IRS can quickly and accurately determine if a taxpayer claiming the earned income tax credit (EITC) provides the required SSN by cross checking that number with Social Security data. In these cases, math error authority is not only cost effective, but helps those taxpayers who do not need to provide additional information or recalculate any tax benefit since the IRS can do it for them.

In complex situations, when an error is not readily apparent, or when there is no other reliable government database to confirm information, math error authority can increase administrative burdens on taxpayers, or even deny them their due benefits.

That could have happened in the early 2000s with the EITC. The Economic Growth and Tax Relief Reconciliation Act allowed the IRS to use the Federal Case Registry of Child Support Orders (FCR) to deny the EITC to taxpayers if the FCR indicated the claimant was a noncustodial parent. The rationale seemed straightforward: A noncustodial parent, identified by the FCR, probably did not live with the child for more than six months of the year, as required by law (the EITC “residency requirement”).

But family situations can be complicated and don’t always align with custodial agreements in a database. An IRS report found that using the FCR for math error authority would have resulted in a high percentage of“false positives,” incorrectly identifying noncompliant taxpayers. Because of this, the IRS never used the FCR under math error authority to confirm the EITC’s residency requirement.

In the past, the IRS and Treasury have asked Congress to expand math error authority. And IRS may wish to have more authority in the future since the agency has announced it intends to limit audits, especially among lower-income and vulnerable taxpayers.

But even if math error notices are changed or improved—as a result of legislation or agency initiatives—math error authority should be limited to situations that the IRS can accurately and efficiently verify. Otherwise, taxpayers would lose valuable protections.