More than 90 percent of the benefits of a House proposal to temporarily amend the $10,000 cap on state and local tax (SALT) deductions would accrue to households making between $200,000 and $1 million, according to a new TPC analysis.

Soon after the House passed the Tax Relief for American Families and Workers Act of 2024, lawmakers teed up a vote on another piece of tax legislation: the SALT Marriage Penalty Elimination Act. The current $10,000 cap is the same for both single and joint filers, creating a potential “marriage penalty.” The proposal would allow married couples filing jointly and with adjusted gross income (AGI) of less than $500,000 to deduct up to $20,000 for tax year 2023.

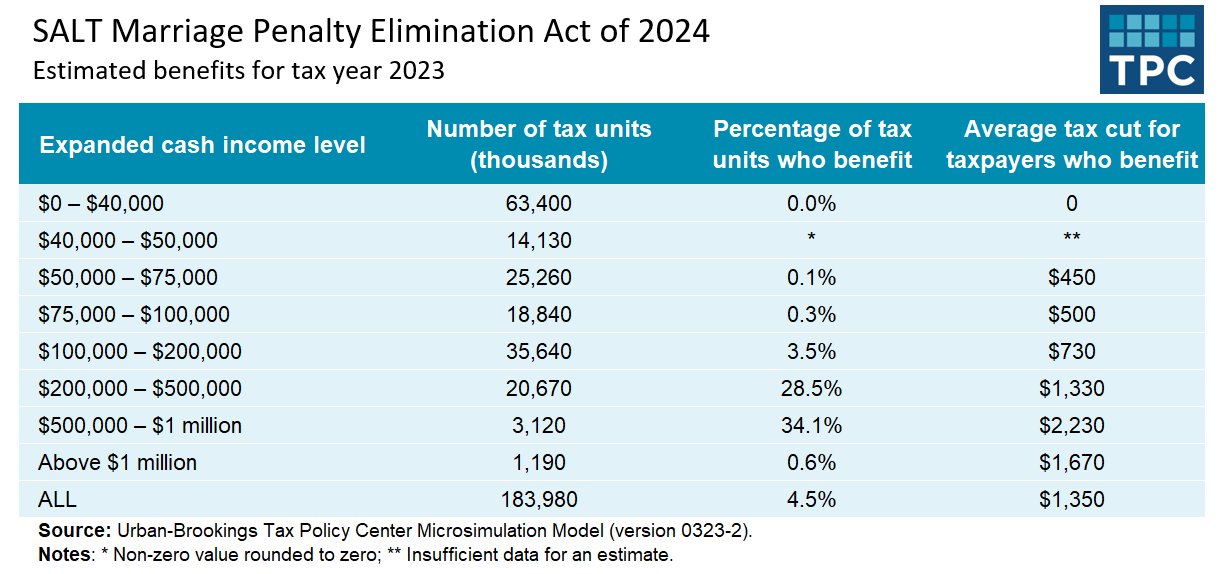

Prior efforts to raise the cap have stalled, due to both the fiscal cost and projections of who would benefit. This legislation calls for a more narrow adjustment that would only apply to an estimated 4.5 percent of households. But, similar to other SALT cap relief plans, higher-income households would be the primary beneficiaries.

Supporters of the bill from high-tax states have argued the tax relief will benefit middle-income households. But fewer than 1 in 1,000 households making below $100,000 would qualify for a tax cut under the plan, according to TPC’s model estimates. For households with expanded cash income between $200,000 and $500,000, 29 percent would get a tax cut averaging $1,330. Thirty-four percent of those making $500,000 to $1 million would also benefit, by an average of $2,230. (TPC estimates show benefits accruing to households with over $500,000 in income because our model uses a more expansive measure than AGI; see this discussion for details).

The proposal would also create a temporary tax cliff that could prompt taxpayers to adjust their behavior to stay under the proposal’s income cap. Because the entire tax benefit is zeroed out when AGI reaches $500,000, taxpayers just above that threshold could face a sizable drop in after-tax income if their pretax earnings rose to or above that limit.

As a result, an eligible household with an AGI of $499,500 would end up with more after-tax income than another making $500,000. Previous SALT cap plans have called for an income phaseout to help avoid this cliff effect.

While congressional action on the SALT cap has been in a holding pattern, many states have adopted taxes on pass-through businesses to allow those business owners and shareholders to bypass the $10,000 cap. Preliminary estimates suggest the state workarounds are already costing the federal government billions of dollars in revenue. These TPC model estimates account for the effects of state SALT cap workarounds.