American wealth has grown remarkably over the last 25 years, with household net worth climbing from $47.5 trillion in 1997 to $139 trillion in 2021 (in 2021 dollars)—an increase from 256 percent of gross domestic product (GDP) in 1997 to 424 percent over the same period.

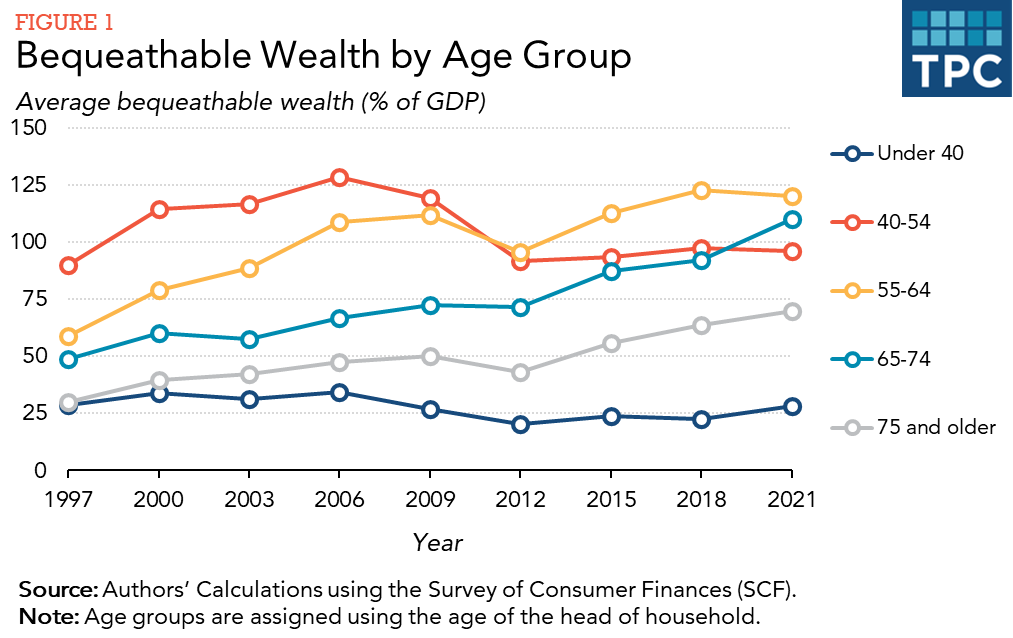

Equally remarkably, households headed by people aged 55 and older have enjoyed almost all (97 percent) of this growth (see Figure 1), and 75 percent occurred in the wealthiest 10 percent of households aged 55 and older. Both the number of households and wealth per household among households aged 55 and older have increased faster than in the rest of the population. As a result, the US can expect the largest flows of intergenerational wealth transfers over the next several decades in modern history, and a substantial share of that wealth—especially among the very wealthiest households—will be passed down within families in a way that maintains family dynasties and increases wealth inequality.

Taxing these flows of wealth judiciously could raise revenue while improving equity among taxpayers and boosting their economic mobility. But the estate tax, the traditional way to tax such transfers, has been eviscerated in recent years. It exempts so much income and contains so many loopholes that only 1 in every 1,300 estates pay the tax. Given the impending wealth transfers and the emaciated nature of the estate tax, wealth transfer taxes are of current policy interest. In recent policy proposals by seven think tanks to address the long-term fiscal imbalance, all seven proposed some reform of the taxation of wealth transfers.

Our new study provides both new methodology for studying transfer taxes and new results. No data set has information on both bequests (what a person leaves to another) and inheritances (what a person receives from another). We adapt by estimating bequests and inheritances via independent methods using the SCF. The methodology does not require that the two estimates be equal, but they turn out to be close both in their aggregate and distribution. We can examine wealth transfer taxes from the point of view of the donor or the recipient, though in this initial project, we analyze all options assuming that heirs bear the burden of the tax (following work by other scholars).

We examine several policies—including inheritance taxes and taxing unrealized capital gains at death. In this brief, however, we focus on reforming the estate tax. In 1972, 6.5 percent of decedents paid estate taxes, generating 0.4 percent of GDP in revenues. By 1997, only 2.1 percent of decedents paid estate taxes, equaling just 0.19 percent of GDP. And by 2021, the tax raised just $18 billion, or 0.08 percent of GDP, in revenue.

We show that, if the estate tax had remained in its 2001 form and been indexed for inflation, it would have raised an estimated seven times as much revenue in 2021, or $145 billion. The weakened estate tax cost the federal government significant revenue, especially given how substantially the ratio of bequeathable net worth to GDP grew over this period.

As policymakers look for ways to address large and persistent federal deficits, shoring up the estate tax should be under consideration. It could generate more federal revenue, boost taxpayer equity, and improve economic mobility.