Families benefit from multiple overlapping provisions in the tax code. Over the years, policymakers and analysts have proposed to consolidate and simplify these benefits, applying federal budget savings to a higher tax credit for young children.

The Family First Act (FFA), introduced in April 2025 by Rep. Blake Moore (R-UT) and Sen. Jim Banks (R-IN) continues this approach. Building on an idea outlined by former Sen. Mitt Romney (R-UT) in early 2021 and proposed in 2022 as the Family Security Act 2.0, the FFA would dramatically expand the child tax credit (CTC)—most significantly for children under age 6— and create a credit for pregnant mothers. To offset most of the cost, the bill would reduce, eliminate, or combine other benefits delivered through the tax system, many of which affect families with children.

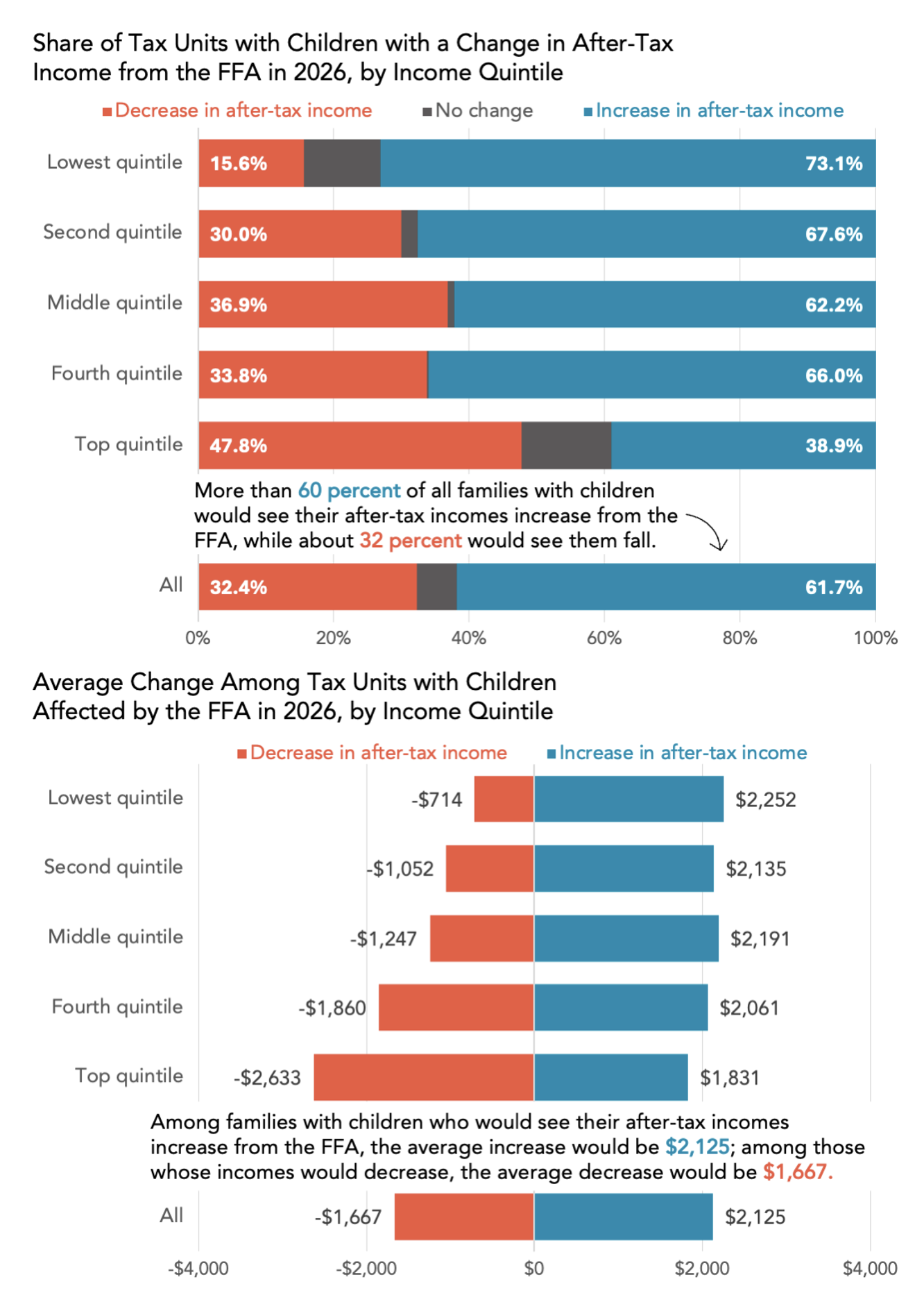

TPC estimates that under the FFA, 62 percent of families with children would see an average increase in their after-tax income of about $2,100, largely driven by the CTC expansion. At the same time, changes to other benefits mean that 32 percent of families with children would see an average decrease in their after-tax income of about $1,700 (Figure 1).

FIGURE 1

Most Families with Children Would See Their After-Tax Incomes Increase Under the Family First Act, with Average Benefits Similar Across Income Levels

Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0325-4) Table T26-0016.

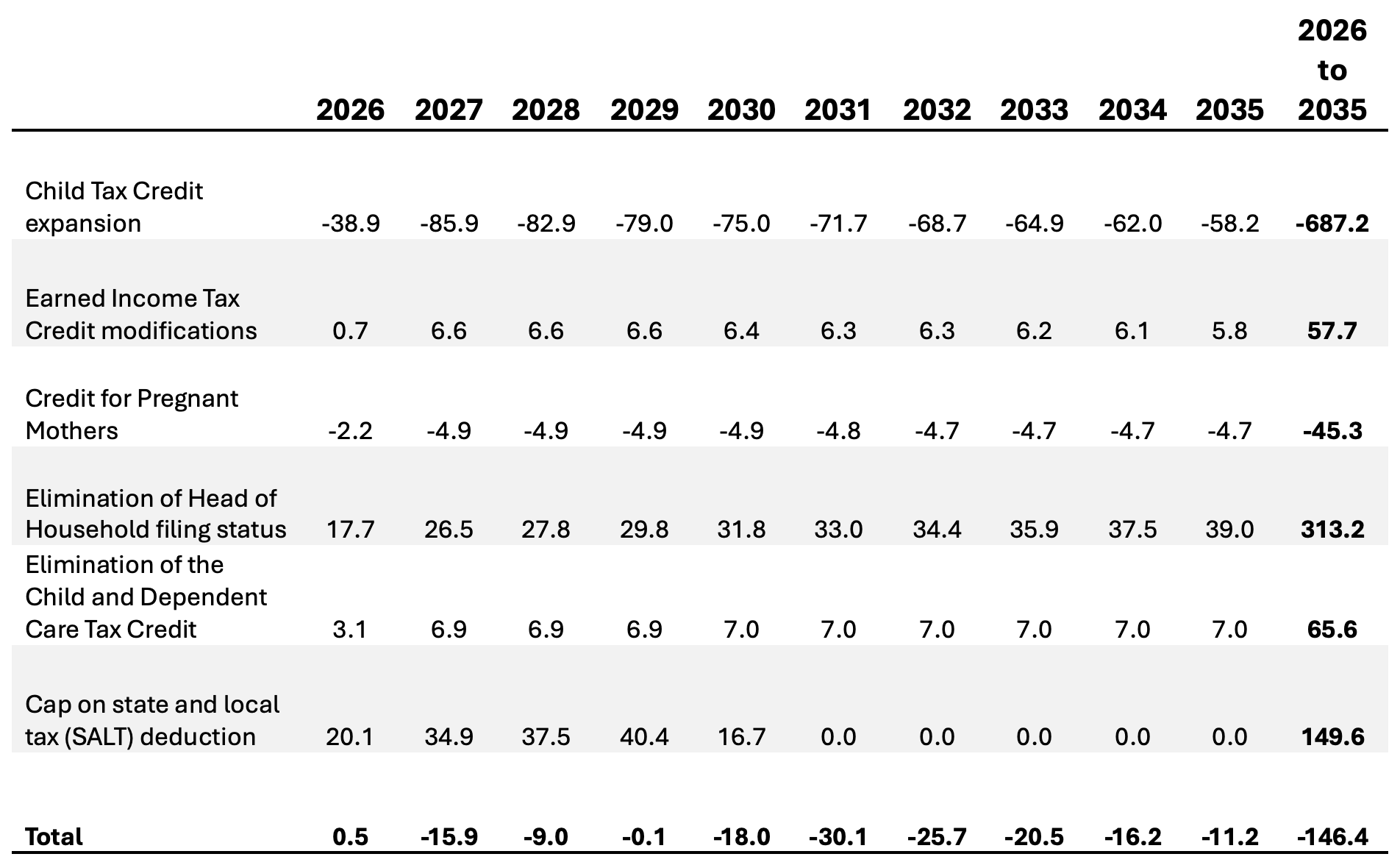

The bill’s CTC changes would cost almost $690 billion from FY2026 – FY2035 but would be largely offset by other provisions in the bill, bringing the net ten-year cost to about $150 billion.

How would the FFA work?

The FFA would provide a maximum CTC benefit of $4,200 for young children (under 6 years old) and $3,000 for older children (6 to 17 years old), up from the current maximum of $2,200 per child under age 17. The bill would establish a new credit for pregnant women of up to $2,800 per fetus with gestational age of 20 weeks or more. No parallel credit for pregnancy exists now.

The bill would offset some of the CTC increases by paring back the earned income tax credit (EITC) for parents of children under 19. It would apply the same EITC formula for families with children under 19 irrespective of the number of children, rather than providing a larger credit for larger families as under current law. This would save about $58 billion from FY2026 – FY2035.

The bill would eliminate two other credits: the child and dependent care tax credit (CDCTC) for families with children (saving about $66 billion over ten years) and the credit for other dependents (primarily benefitting children age 17 to 18 or full-time students age 19 to 23 – savings from this are included in the cost of the CTC).

The FFA would also change two code provisions: Head of household filing status (used primarily by single parents) would no longer be available, and there would be a limit to the amount of state and local tax that can be deducted when itemizing deductions on a federal income tax return. These provisions would save roughly $310 billion and $150 billion, respectively from FY2026 – FY2035.

TABLE 1

The Family First Act Would Cost $150 Billion Over 10 Years, Largely Driven by the CTC Expansion

Budgetary changes of Family First Act provisions, FY 2026–35, in billions of dollars ($)

Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0325-4) Table T26-0014.

Notes: The CTC expansion includes the repeal of the credit for other dependents (sometimes called the other dependent tax credit or ODTC). Each row in the table shows the marginal effect of the change, assuming the preceding rows have been implemented.

Larger child credits for young children would help many, but other changes leave some families worse off

Early childhood is a critical period of development, laying the foundation for lifetime skills, behaviors, and health. It’s also a time when many parents, especially women, struggle to balance work and caregiving.

Boosting credits for young children, as was done temporarily in 2021, can support both child and parents. Other bills, like the American Family Act and the Working Parents Tax Relief Act, would also provide higher benefits for families with younger children.

Researchers have frequently proposed simplifying tax benefits for families, since families must navigate different eligibility rules for the same child. Confusion around claiming benefits can mean families do not understand which children are eligible for various benefits. That can reduce participation by eligible families and contribute to errant credit claims by others.

For many families, the FFA would consolidate several benefits and boost their incomes. Almost three quarters of families with children in the bottom 20 percent of the income distribution would see an average increase in their after-tax income of about $2,250 (Figure 1). Almost 40 percent of families with children in the top 20 percent of the income distribution would see their after-tax income rise by an average of about $1,830.

Unmarried parents would be more likely to see their after-tax income drop than married parents. Among families with children in the lowest income quintile who would see their after-tax incomes fall, more than 9 in 10 would be unmarried. The larger CTC would not offset the loss of head of household filing status.

An evolving family tax policy landscape

Other recent proposals have also focused on families with young children. Policymakers may continue to introduce similar proposals in coming years given national concerns about affordability, with varying emphasis on what tax benefits are eliminated to offset some or all costs.