Extending expiring provisions of the Tax Cuts and Jobs Act (TCJA) would cost over $4 trillion through 2035. Most benefits would go to the wealthy, and limited benefits would reach working families—many of whom are struggling to pay for the basics.

But as I explore in a recent paper, there are less costly alternatives to simply extending the TCJA that provides substantially more benefits for the working class. I propose an alternative that builds on TCJA’s tax simplification gains and shores up the finances of working families by focusing on refundable tax credits.

Consider this proposal

Because of the design of our tax system, many working class families with modest incomes owe little to nothing in federal income taxes (although they do pay other taxes, especially payroll taxes, on their earnings). That means cutting marginal tax rates, as the TCJA did, or exempting certain types of income from taxation like tips or overtime, as President Trump proposes, provides them little to no tax benefit.

But these families can benefit from refundable tax credits — credits where taxpayers receive the full value even if they owe very little in income taxes.

My proposal would:

- Retain the TCJA’s larger standard deduction and repeal of personal exemptions (including for dependents)

- Let most of the other temporary provisions of the TCJA expire, since they provide limited benefit to families at the lower end of the income distribution

- Reform and expand the earned income tax credit (EITC) and child tax credit (CTC) into distinct worker and child credits

Under this plan, a new worker credit of up to $2,500 for workers earning at least $10,000 annually would replace the EITC. The new child benefit credit would deliver a benefit of up to $4,000 per child for households with at least $10,000 in annual earnings.

The first half of the child credit—$2,000 per child—would be available to families irrespective of their earnings. The second half of the child credit would be phased in proportionally over the first $10,000 in earnings, effectively phasing in the credit faster for larger families similar to a bipartisan tax deal that passed the House but stalled in the Senate last year.

It focuses on people with modest incomes

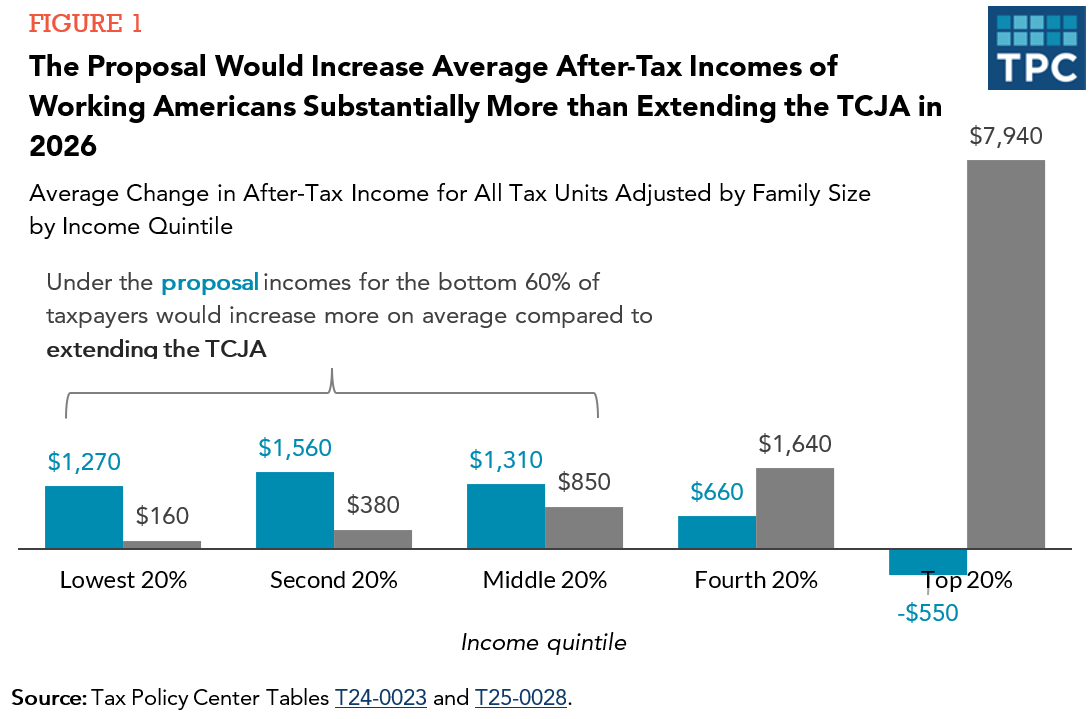

Unlike simply extending the TCJA, this proposal focuses its benefits on working families with low and moderate incomes, especially those with children. In 2026, almost all of its benefits go to the bottom 60 percent of households. Figure 1 shows the proposal would increase those households’ after-tax incomes by between $1,270 to $1,560 annually on average.

Among the bottom 60 percent of households with children, after-tax incomes would increase on average by $2,810 to $4,130.

The worker credit would also increase incomes for people with low incomes who are not raising children at home, (some of whom may be financially supporting children living in other households). These workers have historically been excluded from social safety net benefits but can still face significant hardships. And it would minimize marriage penalties faced by some low-income dual income working couples.

It simplifies tax filing and tax administration

Creating distinct work and child benefits would make tax filing simpler for many working families, especially those with children, reducing the number of child related benefits they need to apply for.

Taxpayers with children wouldn’t have to navigate one set of eligibility rules to claim the child for the EITC, only to navigate a different maze of rules to determine if the same child makes them eligible for the CTC. And because the personal exemption including for dependents would be permanently repealed, they wouldn’t have to navigate those eligibility rules either.

The proposal reduces administrative issues faced by the IRS. The agency would no longer have to program their systems for one set of child eligibility rules for one benefit, and a different set of rules for another. These are some of the reasons the National Taxpayer Advocate has recommended creating distinct and rational worker and child benefits.

The idea is not new, and it already has bipartisan appeal

Many aspects of this proposal have been suggested before, and they have bipartisan roots and support. For example, the 2012 Dominici-Rivlin plan included the establishment of distinct worker and child benefits. Speaker Ryan and President Obama both supported expanding tax credits for workers without children in 2014. And on both sides of the aisle, Congress has expressed interest in expanding tax credits for children, as seen in the Family First Act from Rep. Moore (R-UT) and the American Family Act from Rep. DeLauro (D-CT).

As Senator Hawley (R-MO) noted at the beginning of the 119th Congress “[t]he test of this Congress will be whether we strengthen America’s families and whether we deliver for America’s working people.” If Congress simply extends the TCJA, they will fail this test and miss broader opportunities for to address longstanding issues with the complexity and unfairness of refundable tax credits. Fortunately, alternatives exist that deliver for working families while also reducing the overall cost of addressing TCJA’s expiring provisions.